Until recently, when a customer was shopping for a pair of shoes, they typed a query, scrolled through ten links, compared two or three websites, and often ended up discovering a brand they had never heard of. That journey is disappearing. In its place: a single answer, generated by an AI, suggesting two or three products. And now also proposing to buy them without ever leaving the conversation.

This is not just an interface detail (an “AI overview” link, for example). It is reshaping commercial visibility in a way that is even more brutal than Google Ads or the rise of marketplaces did in their time.

For small brands and local retailers, who have already lived through two decades of a steadily shrinking window of exposure, this is a third wave. Probably the toughest one yet.

This article tries to map out what is taking shape: the recent deals between AI giants and commerce giants, the mechanism by which results are getting impoverished, and the central question - what space is left for those who are neither Amazon, nor Walmart, nor one of the million merchants tied (and beholden) to Shopify?

1. Before AI, a funnel that was already narrowing

To understand what is happening today, you have to remember where we came from.

For twenty years, an online retailer’s visibility rested on two pillars: organic ranking on Google, and presence on a handful of marketplaces. Both have gradually shifted toward a toll-based logic.

On Google, the share of screen reserved for organic results has shrunk as sponsored ads, Shopping, local pack blocks and featured snippets occupied the top of the SERP. On marketplaces, the math is plain: Amazon typically takes 8% to 15% in referral fees on third-party sales (depending on category), plus fulfillment fees, and Sponsored Ads has become a near-mandatory budget just to surface in the first results.

For a local or independent brand, the math was already tight. But at least there was an exit: a motivated customer could still, by typing the exact product name or clicking an organic link, land directly on the merchant’s site, without intermediation. That exit is closing.

2. The shift to zero-click

The first shock, already measurable, is the one caused by AI Overviews and, more broadly, generative search. The data accumulating over the past eighteen months all tells the same story.

According to Ahrefs, the presence of an AI Overview at the top of the SERP correlates with a 34.5% drop in average CTR on top-ranked pages (the AI-generated summary absorbs the query and the content is consumed without the user ever visiting the source). A BrightEdge study published in May 2025 puts the average CTR drop at 30% since AI Overviews started rolling out in Q1 2025. Pew Research, relayed by Ars Technica, talks about nearly 50% fewer clicks to external sites when an AI Overview is present.

The phenomenon is now massive: 58.5% of Google searches in the US end without a click, and according to consulting firm Bain & Company, 80% of consumers rely on zero-click results at least 40% of the time, with overall organic traffic down by 15 to 25%. Forrester measures a 10% decline in organic traffic to US websites over the single 2024-2025 year.

Some sectors are hit harder than others. According to data compiled by Dataslayer and The Digital Bloom from the March 2025 core update, queries triggering an AI Overview have exploded in entertainment (+528%), restaurants (+387%), travel (+381%), real estate (+258%) and transport. News publishers are taking part of the hit at the end of the chain: 37 of the 50 largest US news sites saw their traffic decline year-over-year in May 2025, with CNN losing between 27% and 38% depending on the measurement window.

For a small retailer, this means two very concrete things:

- Informational queries around their products (“what’s the difference between this and that material”, “how do I choose …”) no longer generate visits. The answer is given in the AI Overview, and the educational content the retailer invested in now serves as raw material for the AI, with no traffic in return.

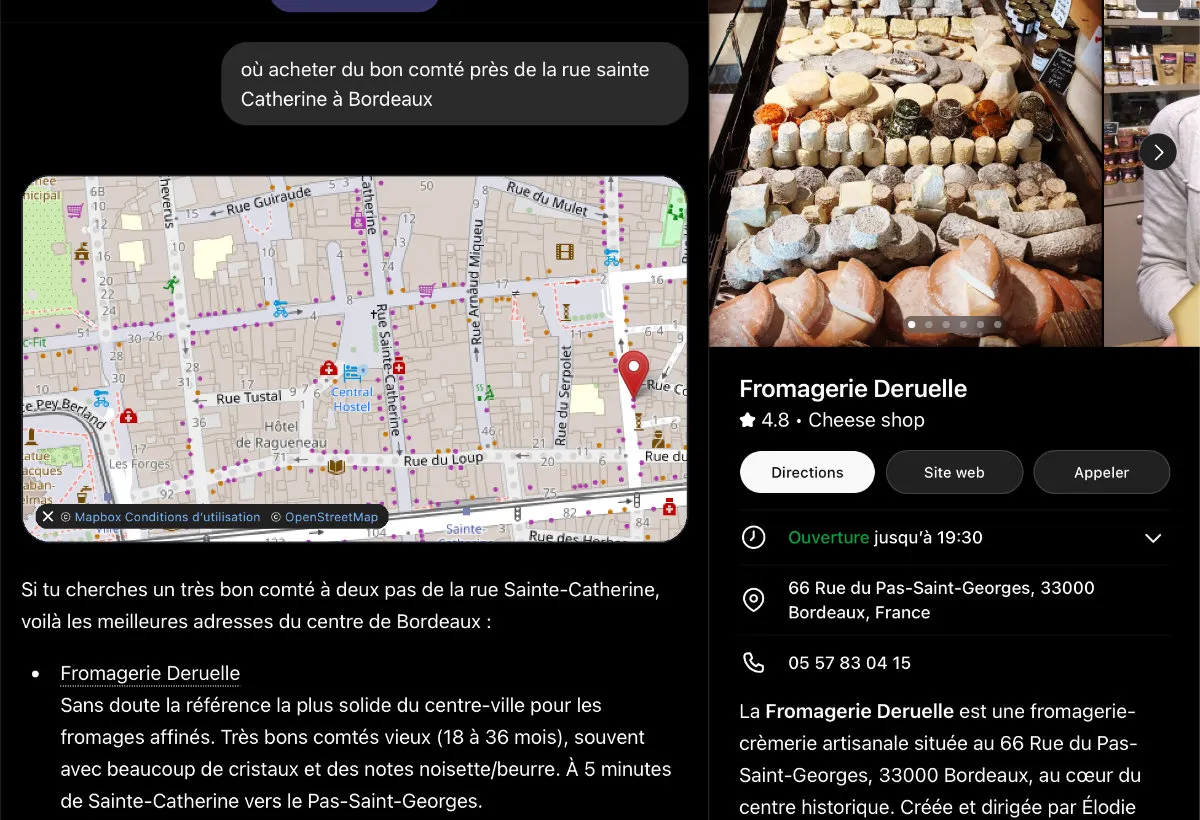

- Local queries (“best cheesemonger near me”, “where to buy cheese in Bordeaux”) are now massively absorbed by AI Overviews. Visibility no longer depends on local SEO in the classic sense, but on the consistency of data between the Google Business profile, the website, and directories - a different kind of work, and one that few small retailers have structured.

3. Agentic commerce: what the giants just locked in

In this already strained context, a second wave is arriving, more directly transactional: agentic commerce. The idea - an AI agent that doesn’t just recommend but actually buys on your behalf - had been on the drawing board for a while. It became industrial reality in the autumn of 2025.

Kickoff: September-October 2025 with Instant Checkout

On September 29, 2025, OpenAI announced Instant Checkout inside ChatGPT, in partnership with Stripe. The first integrated merchants were US Etsy sellers, with over a million Shopify merchants soon to follow: Glossier, SKIMS, Spanx, Vuori, Steve Madden, and so on. The underlying protocol, the Agentic Commerce Protocol (ACP), was published as open source.

Two weeks later, on October 14, 2025, Walmart announced a deal with OpenAI. The largest US retailer joined the ChatGPT Instant Checkout ecosystem. Its CEO, Doug McMillon, declared that the e-commerce experience “consisted, until now, of a search bar and a long list of answers” and was about to change.

On January 11, 2026, Shopify and Google in turn announced the Universal Commerce Protocol (UCP), co-developed between the two companies, already backed by more than 20 retailers and platforms. Shopify merchants can now sell directly inside Google Search AI Mode and inside Gemini. And Microsoft Copilot announced a similar integration.

The volumes are massive. According to Adobe Digital Insights data cited in March 2026, AI traffic to retail sites grew 4,700% year-over-year by mid-2025. Shopify reported that AI-attributed orders on its platform were multiplied by 11 between January 2025 and January 2026. OpenAI claims 2.5 billion daily prompts, of which 2% are shopping-related - 50 million purchase queries a day, across 700 million weekly users.

The Instant Checkout failure… six months later

And yet, in late March 2026, OpenAI quietly shut Instant Checkout down [1]. The reasons are both technical and structural. Technically: OpenAI was relying heavily on scraping to obtain product data, producing stock, price and delivery information that was frequently inaccurate. Emily Pfeiffer, principal analyst at Forrester, put it plainly: crawling and scraping are not enough to provide the data depth required for a satisfying shopping experience.

Structurally: an initial promise of “a million Shopify merchants” against the reality at the time of the wind-down - around 30 merchants available through Instant Checkout. Walmart had put 200,000 products online, which is a lot, but nowhere near enough to cover a modern retail catalog. And most importantly, conversion rates were three times lower than for a purchase finalized directly on the retailer’s site. An Adobe-Semrush study from March 2026 surveying over 1,000 US consumers confirms the trend: only 22% of users have ever bought directly inside an AI tool, while 50% report having made a purchase after using AI to do research. Chatbots have become powerful discovery tools, not finalization tools.

The new model taking shape has a name: “ChatGPT Apps”. Each retailer builds its own agent and plugs it into ChatGPT. Walmart pushes Sparky directly inside ChatGPT and Google Gemini. Etsy is building its own ChatGPT app. Shopify confirms that its merchants will remain visible in the chatbot, but that payment will happen on the merchant’s store, no longer in the chat. The general idea is now: own the agent, rent the distribution.

This first phase of agentic commerce, rather than disintermediating, revealed a different truth: no player has cracked the formula yet. The episode is worth remembering, not because it buries agentic commerce for good, but because it illustrates how fast a channel can appear, dominate the entire industry conversation, then vanish in six months. For a merchant who would have built their strategy on Instant Checkout between October 2025 and March 2026, returning to square one is a warning.

The Walmart pivot: piloting the new model

Walmart became, in this episode, the clearest illustration of the new model. Rather than letting OpenAI handle the transaction, the retailer slots its own in-house agent, Sparky, directly into ChatGPT and Google Gemini. Walmart pays a flat API fee to OpenAI, not a revenue share. And the early numbers back the choice: according to Walmart, users going through Sparky inside ChatGPT complete purchases at around 70% of the rate observed on Walmart.com directly. A result well above Instant Checkout’s.

This model reveals an asymmetry: only the very largest can afford an in-house agent. Building a Sparky is not within reach of an average Shopify merchant. And even though Shopify announced that its merchants would stay visible inside ChatGPT without specific development, the bargaining margin on terms remains, by design, between Shopify and OpenAI. Not the merchant.

The Amazon vs. Perplexity battle: the other side

While Shopify, Walmart and Google enter OpenAI’s game, Amazon is playing exactly the opposite strategy: lock down its own territory.

In November 2025, Amazon sued Perplexity. The reason: Perplexity’s Comet browser was shopping on Amazon on behalf of users, and allegedly disguised its automated sessions as standard Chrome sessions to bypass Amazon’s technical blocks. On March 9, 2026, the federal judge for the Northern District of California granted Amazon a preliminary injunction barring Comet from accessing password-protected Amazon accounts and ordering the destruction of collected data.

Amazon has reportedly blocked dozens of external agents from its platform, including ChatGPT, while building its own assistant Rufus, which generated close to 12 billion dollars in annualized incremental sales in 2025. Rufus claims 250 million users in 2025 and a conversion rate 60% higher than standard journeys.

On May 13, 2026, another turn: Amazon announced it would discontinue the Rufus chatbot as a standalone product to integrate its capabilities directly into a new Alexa-based shopping agent, inserted into the site’s search results. The calculation is clear: use the most valuable real estate on the site (the first search results, until now monetized as Sponsored Products) to push an algorithmic recommendation.

And in February 2026, Amazon invested 50 billion dollars in OpenAI. What looked like a war is starting to look more like a cartel.

4. The hidden passage: a new layer of intermediation

Here is what is not said clearly enough: AI does not disintermediate, it re-intermediates.

In January 2026, it was reported that OpenAI planned to take a 4% commission on each Shopify sale made through Instant Checkout. On top of that commission, the usual Shopify fees (subscription + ~2.9% processing). For a merchant selling via ChatGPT, the cumulative cost could approach 6.9 to 7.5% per transaction, not counting the upstream cost of optimizing products to be readable by the AI.

That commission was never applied at scale, since Instant Checkout was shut down a few weeks later. But the published figure is worth remembering: it’s the order of magnitude OpenAI was banking on to monetize the channel. As soon as the next model (ChatGPT Apps, in-house agents plugged into ChatGPT) finds its economic formula, this will be the starting point of negotiation. The pressure toward paid intermediation has not been neutralized by the technical end of Instant Checkout - it has only been postponed.

For comparison, Amazon takes 8 to 15% on third-party sales, eBay around 10%. A new 4 to 7% take, in this landscape, would be neither absurd nor prohibitive. But it is one more dependency on a single actor, whose pricing terms are opaque today and bound to evolve. OpenAI has mentioned that advertising will eventually be part of the model, putting agentic commerce on the same trajectory as Google Shopping: no preferential placement today, but an in-chat purchase feature that paves the way for an in-chat Google Shopping.

Google AI Mode, for its part, is already testing Shopping Ads inside its conversational interface. The answer to the question “will the channel be paid?” is therefore already known: yes, in the near future.

5. The impoverishment of results

Beyond the economic angle, there is a more insidious effect: the very nature of the answer narrows the range of choice.

Popularity bias, laid bare

Academic research on recommendation systems has long identified “popularity bias”: algorithms surface what is already well-known, at the expense of the long tail. LLMs amplify this bias. Several recent studies [2] show that GPT models over-represent popular items in their recommendations, even when diversity is explicitly requested in the prompt.

The reason is mechanical. An LLM learns statistical frequency. The more a brand is cited in its training corpus, the more likely it is to appear in the answer. A local brand mentioned ten times on the web stands no chance against a brand cited ten thousand times. Older work on the unfairness of popularity bias in recommendation systems had already put it bluntly [3]: a market dominated by this bias mechanically concentrates attention on a few well-known brands, at the expense of diversity and innovation.

Three links become one

The funnel effect is arithmetic. Where a Google SERP offered ten clickable organic results, plus Shopping results, plus a Maps card, an AI Overview offers a single synthesis. Where ChatGPT today recommends three or four products, the models taking shape (in-house agents inside ChatGPT, Gemini integrations, AI Mode) all aim for the same contraction of choice: a short, pre-filtered selection, with or without native transaction.

Anne-Claire Baschet, Chief Data & AI Officer at Mirakl, puts the diagnosis without ambiguity:

The consequence: if a brand is not in the two or three suggestions retained by the AI, it does not exist.

The loop effect

On top of that, a second-order effect [4]: as the web fills up with content itself generated by AI (product descriptions, blog articles, comparison pages), future models will increasingly train on AI-generated content. Researchers are starting to talk about informational waste [5] to describe this mass production of normalized, low-trust, low-value content that dilutes the global value of the information available on the Web. The risk is a leveling: everyone ends up describing their products with the same phrasings, the same arguments, the same attributes. The singularity of a local brand (its voice, its way of telling its story) becomes unreadable to the machines that filter choices.

An intelligence with no anchoring, no responsibility

One thing to keep in mind in the background. AI is an intelligence, in the sense that it processes, synthesizes, recommends - and does so with a speed and reach no human can match. But its difference from a human is not only quantitative. It is also qualitative, and deeply asymmetric: it is anchored in no real world, and it has no act to account for.

Information science researcher Arthur Perret has formalized this intuition [6]. His thesis, building on foundational work on the document as a regime of truth (Buckland, Briet, Otlet): LLMs are communication machines, not information machines. They know only relations between words, not relations between words and things. Where a product page written by a merchant is a document (in the technical sense of evidence supporting a fact), an LLM’s reply is a plausible utterance, with no value as proof, reference or testimony. Perret describes the shift as moving from a documentary regime of truth to a regime of verisimilitude.

A widely cited paper [7] goes further, mobilizing the notion of bullshit: not lying (which would presuppose an intent to deceive) but indifference to truth. The authors summarize: LLMs do not perceive, so they cannot misperceive; the fact that they get things right is only an indirect byproduct of their operation. The machine produces statistically plausible discourse. Whether that discourse is true or false is incidental from the point of view of the system.

In passing, Perret notes shrewdly that calling these systems’ errors “hallucinations” is a rhetorical convenience: it suggests the machine normally tries to tell the truth and occasionally goes astray. This rhetorical move is not new. Google had long made “the algorithm” an autonomous actor behind which editorial choices became unchallengeable (“it’s not us deciding, it’s the algorithm”). With LLMs, the same sleight of hand plays out, all the more effective because the system is even more opaque: calling “hallucination” what is in fact the standard mode of operation of the device is to turn the error into an accident along the way rather than a feature of the device itself - and to escape the burden of justification.

When an independent cheese shop in Bordeaux recommends a Comté, the cheesemonger has tasted it, aged it, negotiated its price with a producer they know, and is well aware that an unhappy customer will come back to tell them about it next Saturday at the market. Their recommendation commits them, economically and socially. When an AI recommends a product, it has tasted nothing, spoken to no one, receives no feedback, and if the recommendation is bad, there is no one to address: not the AI, which feels nothing, nor the platform hosting it, which will shield itself behind its terms of service. The risk is fully transferred to the retailer at the end of the chain and to the consumer.

This asymmetry has two practical consequences. First, nothing in how AI works pushes it to arbitrate in favor of the actual quality of a product or service: it arbitrates in favor of what is best documented, best structured, and most statistically frequent in its corpus - which is not the same thing. Second, the only player in the chain still accountable for anything (their reputation, their solvency, their relationship to their customers) is the merchant themselves.

Put differently: in a world where a growing share of choices is made by machines with no anchoring and no consequences, what holds value for the customer is precisely what has those qualities - a human who replies, a store you can walk into, a brand that will repair. This asymmetry is, paradoxically, one of the few solid advantages left to independent retailers.

And the customer themselves is being eroded

A final angle, rarely discussed. The impoverishment doesn’t only affect supply (fewer visible brands); it also affects demand, the cognitive capacities of the consumer themselves.

Several recent studies document the effects of regular LLM use on users’ mental capacities: dependence on the machine and decline in autonomous learning performance [8]; reduced memorization capacity [9]; erosion of critical thinking and reasoning [10]. The mechanism is simple: the more you delegate, the less you train the muscle.

For a retailer, this is a shifting terrain. For twenty years, their customer typed ten queries on Google, compared three sites, read reviews, doubted, came back, compared again. That journey, tedious as it was, was also a journey of empowerment: the customer was forming an opinion, becoming an expert on their own need. It was that journey that made encounters with unknown brands possible, because there was time to doubt and desire to seek out.

With conversational AI, this journey shrinks. The customer asks, the AI replies, the customer buys. The very capacity to compare, to doubt, to seek beyond the first proposal, atrophies as the habit takes hold. The independent retailer is no longer fighting only against an algorithm that doesn’t see them; they’re also fighting against a customer who has lost the habit of searching.

This is probably the heaviest shift of the next five years, and the least discussed at e-commerce conferences. Why? Because we’re rushed by speed and results. Merchants are adapting in the urgency, tossed by a deeper societal shift that goes beyond them. We talk tools, we talk channels, we talk conversions. We don’t talk about the customer who is, also, changing.

6. What room is left for small brands and local retailers?

The picture so far is bleak. But the diagnosis is not only one of indictment.

Several recent studies show that agentic commerce, paradoxically, can rebalance certain cards - provided you understand what is changing.

Local becomes, paradoxically, an advantage

An IBM-NRF study indicates that 40% of consumers already use AI to guide their purchases. Another, less commented figure: more than a third of consumers are already considering using AI to find a local business. And local queries have seen their AI Overview coverage explode (+273% for restaurants). In other words: if you run an independent cheese shop in Bordeaux, the customer is no longer going to type “cheese shop Bordeaux” on Google - they will ask ChatGPT “where to buy good Comté near Marché des Capucins”. The channel changes, but the intent remains. And remains local.

The determinant of visibility, however, is no longer the same. AIs don’t arbitrate on PageRank or keyword density. They arbitrate on the consistency and richness of structured data: up-to-date hours, identical address everywhere, frequent and high-quality customer reviews, clear description, precise attributes (gluten-free, dairy-free, organic certification, local production). It’s a terrain where a good independent cheese shop, meticulous on its Google profile and its website, can beat a big-box store that has neglected its local data.

The dependency trap: don’t replay the Google playbook

For fifteen years, online acquisition relied almost exclusively on Google - not by choice, but because the search engine’s dominance left no credible alternative. The consequence is well known: the day the algorithm changed, or the day cost-per-click doubled, thousands of e-merchants had nothing left to cushion the blow.

Agentic commerce is taking shape on the same mechanism, but with intermediaries that are younger and less regulated. The Instant Checkout episode illustrates the fragility of these channels better than any theoretical argument: announced with fanfare in September 2025 as “the next step of commerce”, buried six months later, in late March 2026. For merchants who had oriented their efforts toward this specific integration, that’s six months of product and communication work called into question.

What this episode confirms:

- pricing terms are opaque (the 4% commission was only revealed after the fact, through a press leak) and bound to evolve;

- advertising will return sooner or later to push some recommendations to the top;

- the feature itself can disappear overnight, even after being presented as a revolution.

The model taking over (“ChatGPT Apps”, in-house agents of large retailers plugged into ChatGPT) does not fix these fragilities. It displaces them. Building one’s own agent (a Sparky, Walmart-style) is not within reach of a merchant who isn’t doing several hundred million in annual revenue. For others, the Shopify solution (visibility without specific development, payment at the merchant’s store) is more accessible. But it remains governed by terms defined between Shopify and OpenAI, with no bargaining margin for the individual merchant. The technological dependency on the solution provider remains very strong and very risky.

What holds, and what gets built

What holds are the channels the merchant controls: their own website, their email list, their community (Instagram, newsletter, local physical community), their store. None of these channels is filtered by an AI agent. A website on Magento Open Source or WordPress, where the merchant owns the code, the database and the customer file, is by design an asset no one can switch off overnight.

What gets built is GEO (Generative Engine Optimization): producing factual, dense content, citable by AIs, structured in Schema.org, with complete product data (materials, dimensions, warranties, certifications, returns). For a merchant, it’s a concrete project: enriching product attributes, polishing pages, structuring customer reviews, publishing editorial content with high factual density. It’s foundational work on data quality.

Finally, there is what Laëtitia Muré, CEO of Feed Manager, calls stepping out of “the brand’s showcase”: accepting that the product page is no longer just viewed by a human visiting the site, but ingested, compared and restituted by an AI. That implies rewriting bullet lists, broadening semantic fields, exposing technical attributes.

7. Conclusion: resilience is an architectural choice

The story unfolding before our eyes is one of a recomposition of the commercial visibility chain. The giants are signing deals among themselves: OpenAI with Stripe, Walmart with OpenAI, Shopify with Google, Amazon against everyone else while it builds its own agent. Small brands and independent retailers, on the other hand, have no seat at the table.

Four useful principles, from the standpoint of a merchant who wants to still exist in five years:

Diversify acquisition channels. Stop depending 80% on a single flow (Google, ChatGPT, Instagram, Amazon). Build the email list, the community, the local partnerships, the physical store where it applies. A proprietary channel is the only one that doesn’t depend on an algorithm change or a new deal between two giants.

Own your tools and your data. Beyond acquisition channels, the question is about infrastructure itself: who owns the website, who hosts the product database, who holds the customer file, who controls the CRM and the automations. Renting one’s commercial tool to a single actor (a SaaS that can change its terms, close an account, raise its prices, restrict data export) means putting oneself in the same dependency as on Amazon or Google, at an even deeper level. Independence from platforms starts with the ownership of tools. It’s less spectacular than an agentic integration. It’s infinitely more solid.

Invest in product data quality. It is now the raw material AIs feed on. A poor product page is an invisible product. A rich page - factual, well-structured, with attributes, reviews and certifications - becomes a competitive advantage.

Refuse absolute platform dependency. Being present in Agentic Storefronts or future ChatGPT Apps may make sense to capture new traffic. But building one’s entire revenue there means putting oneself in the position of those who bet everything on Amazon - and watched their margins melt away when the commission ticked up. It also means taking the risk, as the Instant Checkout episode showed, of seeing the channel disappear in six months.

Agentic commerce is not a fatality of impoverishment. But it is, by design, a mechanism of concentration: fewer proposals displayed, more power to intermediaries, more standardization of answers. It rests a growing share of arbitration on systems that have, themselves, nothing to lose in the operation. For small brands, the point is not to win this battle (they won’t win it head-on); it’s to build a commercial architecture resilient enough so that the gradual loss of the Google channel and the rise of the AI channel don’t, together, prove fatal. And to keep asserting, in the customer relationship, what the machine doesn’t replicate: an anchoring, a presence, an accepted responsibility.

This is probably the conversation to have, in 2026, with any executive who still thinks the subject is purely technical.

Want to build an e-commerce architecture that doesn’t depend on OpenAI’s, Shopify’s or Google’s goodwill?

Let’s talk about your e-commerce strategy

Notes and sources

[1] Sellitto, Johan, OpenAI abandonne Instant Checkout : ce que l’échec du paiement dans ChatGPT révèle, Abondance, March 24, 2026. https://www.abondance.com/20260324-2046117-openai-abandonne-instant-checkout-ce-que-lechec-du-paiement-dans-chatgpt-revele.html. Includes statements by Daniel Danker (Walmart) at the Morgan Stanley conference in early March 2026, analyses by Emily Pfeiffer (Forrester) and Bob Hetu (Gartner), and the Adobe-Semrush study of March 2026.

[2] Di Palma, Biancofiore, Anelli et al., Exploring Diversity, Novelty, and Popularity Bias in ChatGPT’s Recommendations, arXiv, 2025. FairLRM: Bridging Semantic Understanding and Popularity Bias with LLMs, arXiv, 2026.

[3] Abdollahpouri, Burke and Mobasher, The Unfairness of Popularity Bias in Recommendation, DePaul University (Chicago), arXiv, 2019. https://arxiv.org/abs/1907.13286

[4] UCLA Anderson Review, AI from AI: a Future of Generic and Biased Online Content?, January 2025.

[5] Copestake, Duggan, Herbelot, Moeding and von Redecker, LLMs as supersloppers, Cambridge Language Sciences Annual Symposium, 2024.

[6] Perret, Arthur, L’intelligence artificielle générative dans l’impasse informationnelle, 24th SFSIC Congress, June 2025. https://hal.science/hal-05126355 - public version on the author’s blog: arthurperret.fr

[7] Hicks, Humphries and Slater, ChatGPT is bullshit, Ethics and Information Technology, vol. 26 no. 2, 2024. https://link.springer.com/article/10.1007/s10676-024-09775-5

[8] Bastani, Bastani, Sungu, Ge, Kabakcı and Mariman, Generative AI Can Harm Learning, SSRN, 2024.

[9] Abbas, Jam and Khan, Is it harmful or helpful? Examining the causes and consequences of generative AI usage among university students, International Journal of Educational Technology in Higher Education, 2024.

[10] Gerlich, AI Tools in Society: Impacts on Cognitive Offloading and the Future of Critical Thinking, Societies, vol. 15 no. 1, 2025.